The Ocean Floor Is the Cloud:

How Subsea Cables Became the Hidden Backbone of AI

The Internet Has a Physical Address. Own It.

Roughly 99% of intercontinental data travels through glass fibers resting on the seabed. The “cloud” is not in the sky, it is a physical network of cables that four companies are aggressively acquiring. AI has become the marginal buyer of bandwidth, and bandwidth is now the marginal constraint on AI progress.

We believe subsea cable infrastructure represents one of the most durable, mispriced and strategically critical investment exposures of the coming decade.

Three forces are converging:

- Hyperscalers have shifted from tenants to owners, capturing ~71% of global capacity (up from ~10% a decade ago).

- AI workloads, already ~20% of global traffic and requiring 5x the connectivity of traditional topologies, are driving ~30% annual subsea bandwidth growth (Nokia).

- The seabed has become a contested geopolitical domain, with sabotage incidents reshaping resilience priorities.

For institutional investors, this is a barbell opportunity: ownership of the physical layer of the AI economy on one side, and mispriced risks in legacy carriers, exchanges, and sovereigns on the other.

Bottom line: The next leg of the AI trade is not silicon. It is glass. The companies that own the fiber pairs between data centers will earn structural returns the market still prices as a utility expense.

Submarine fiber-optic cables carry 95-99% of intercontinental data and underpin trillions in daily transactions. Satellites are emergency backups only — they cost ~2,800x more per unit of bandwidth and cannot match fiber’s latency or capacity.

Ownership is consolidating rapidly. Google, Meta, Amazon, and Microsoft now account for roughly half of all installed cable capacity worldwide, with their share rising dramatically over the past decade. Investment has nearly tripled in seven years.

Flagship projects include:

- Google’s Equiano (12 fiber pairs, 144 Tbps)

- Meta’s Waterworth (50,000 km, 24 pairs)

- Amazon’s Fastnet (16 pairs, >320 Tbps)

- Microsoft/Meta’s MAREA (up to ~200 Tbps)

AI is the catalyst. Generative workloads demand symmetric, latency-sensitive connectivity. New cables like Meta’s 2Africa (180 Tbps), Candle (570 Tbps), and Fastnet are purpose-built for the inference and training era.

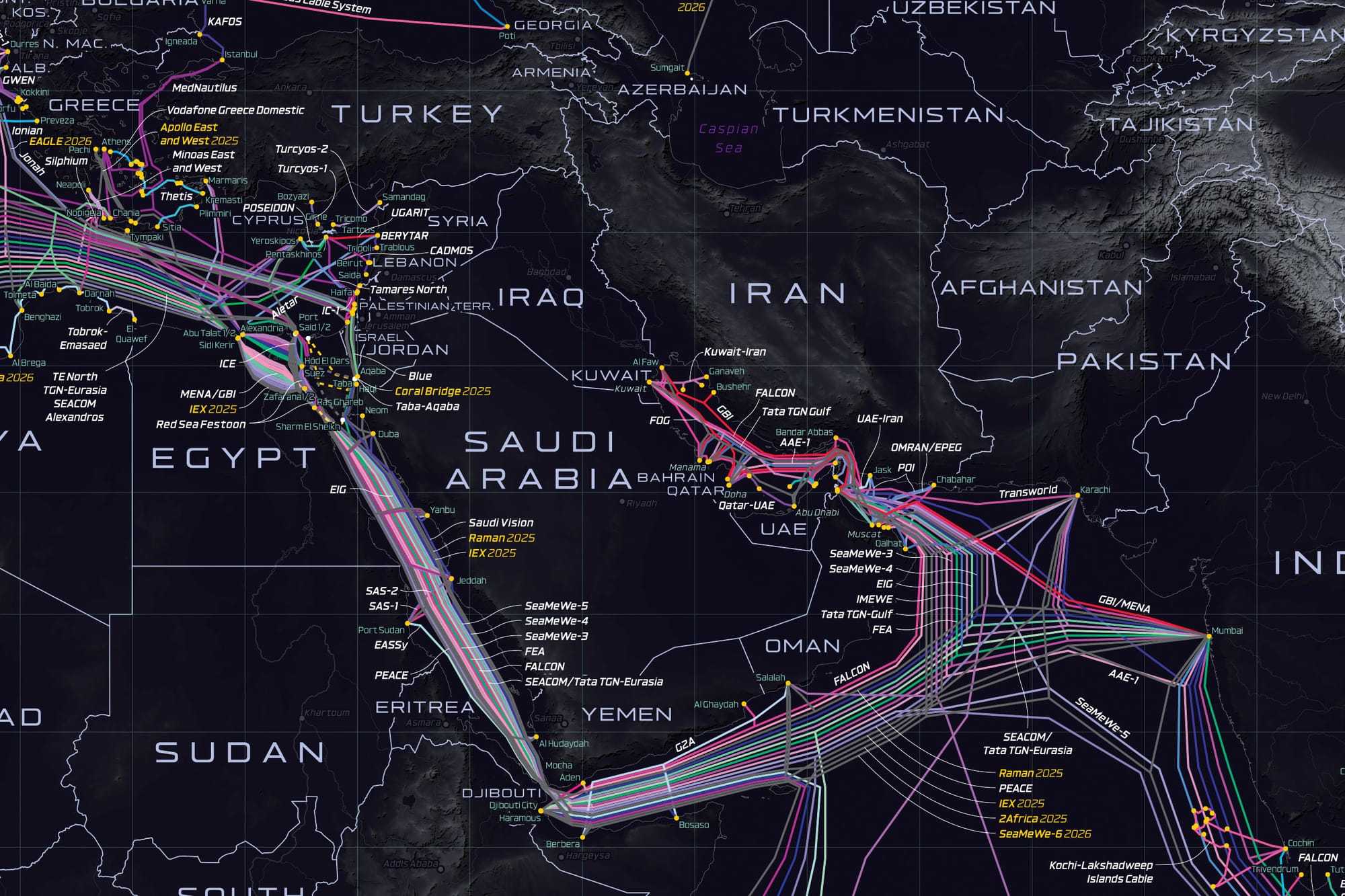

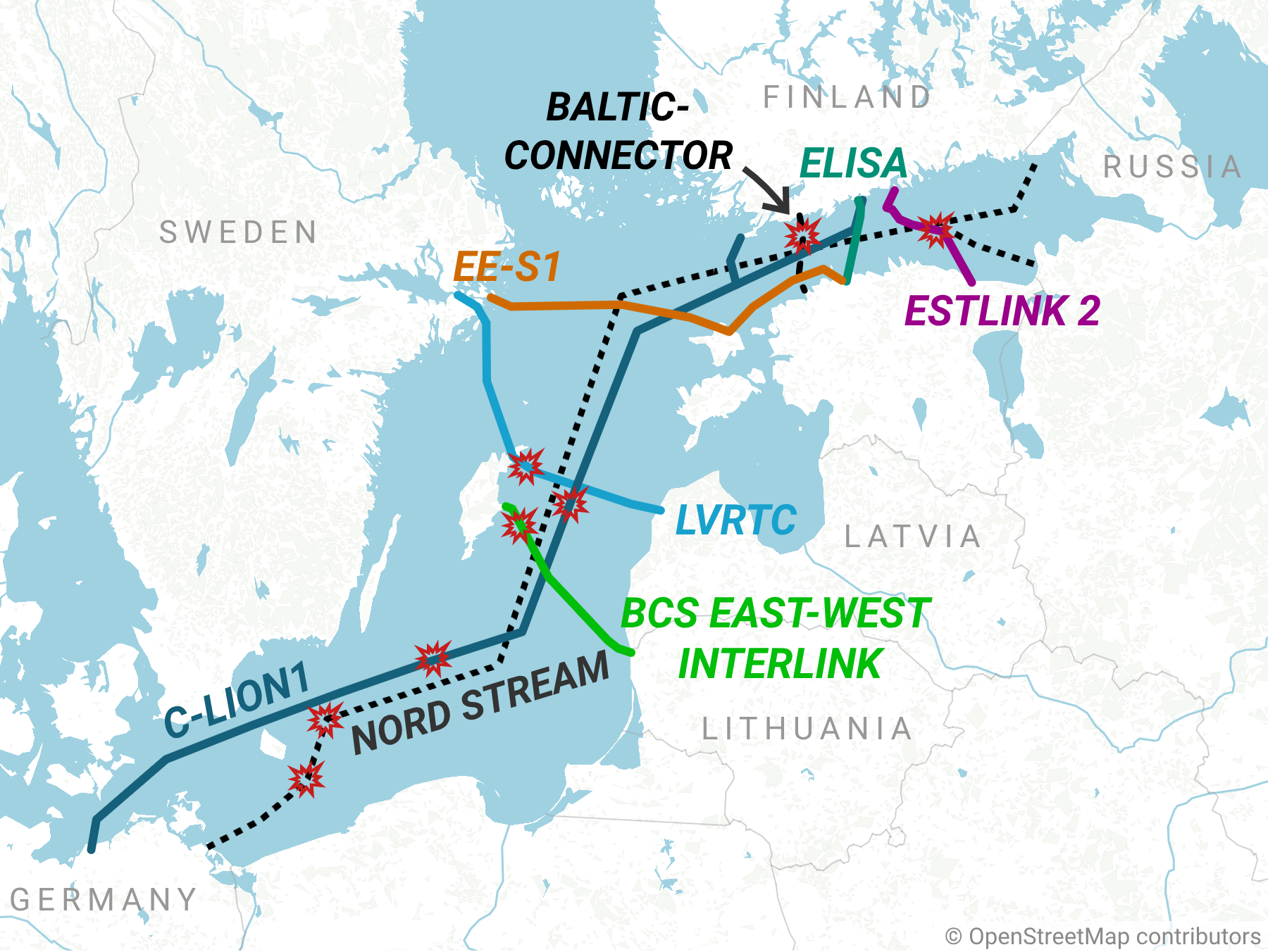

Geopolitical risk is rising. Deliberate cuts in the Baltic, Red Sea, and Taiwan Strait highlight vulnerabilities at five critical chokepoints. National security responses, from NATO’s Baltic Sentry to the EU’s €347 million Cable Security Toolbox, are accelerating.

Five investable consequences:

- Durable moats for hyperscalers

- Pricing power for cable manufacturers (Alcatel, SubCom, NEC ~65% pipeline)

- Second-order gains for optical vendors, marine firms, data-center REITs, insurers, and defense contractors

- Structural risks for legacy carriers and second-tier clouds

- Rising premia for route-concentrated sovereigns and financial venues

The popular “cloud” metaphor hides the physical reality: nearly every intercontinental email, transaction, video, and AI parameter travels through thin strands of glass on the ocean floor.

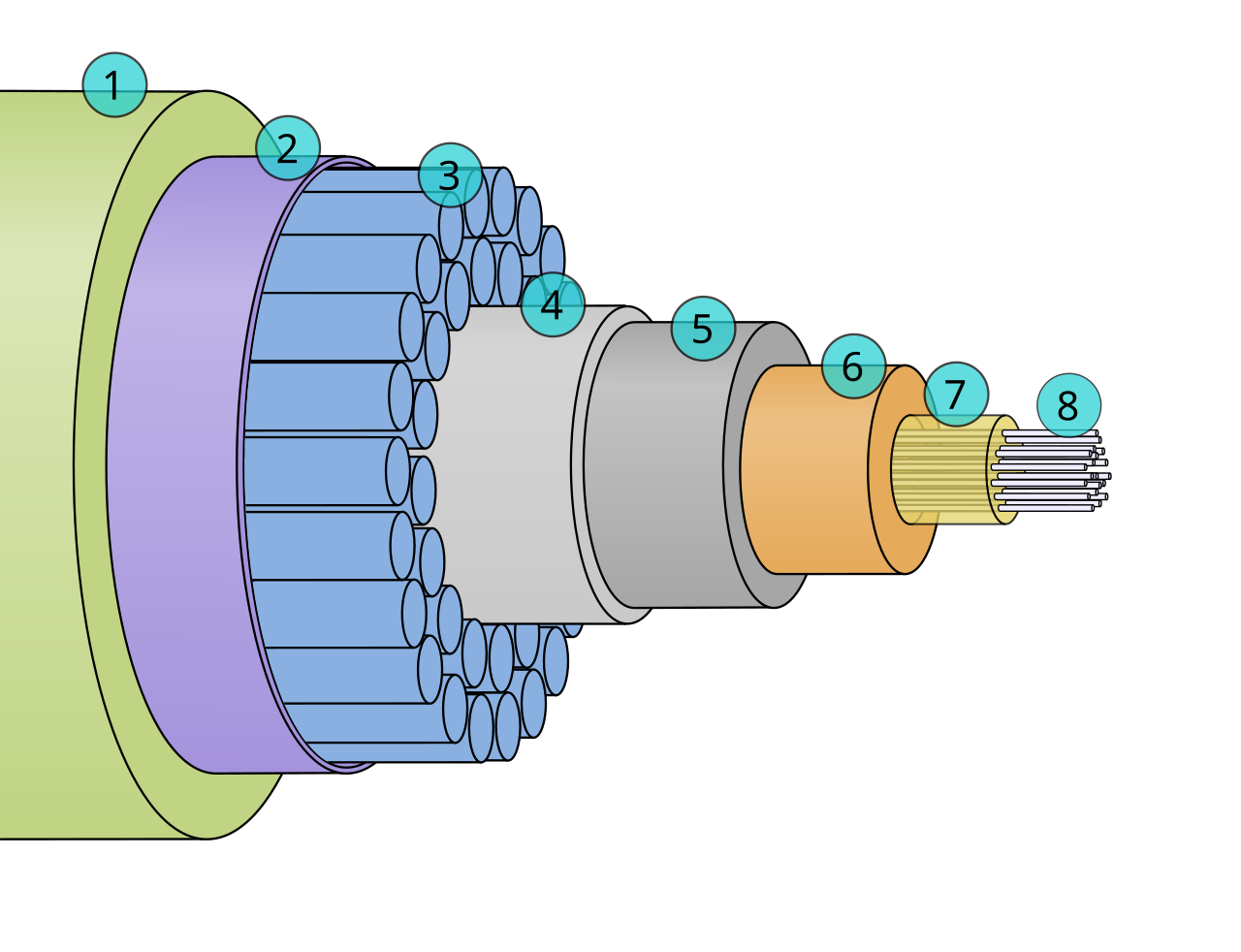

Satellites handle a tiny fraction of capacity at vastly higher cost. Modern cables deliver hundreds of terabits per second with minimal latency. Only ~12% of cable length is buried, yet burial drives ~60% of costs and sharply reduces faults. A fleet of ~62 dedicated cable ships (plus broader repair pool) maintains the network.

Most faults (70-80%) come from fishing gear and anchors. The rest, increasingly deliberate, expose the fragility of global connectivity.

2. Hyperscalers Are Becoming Infrastructure Powers

The old consortium model is being replaced by private ownership.

Alphabet (Google): Over 30 cables, including Curie, Dunant, Grace Hopper, Equiano, and a suite of Pacific systems (Firmina, etc.).

Meta: Leads the most ambitious builds: 2Africa (45,000 km, 33 countries), Waterworth (50,000 km, new corridors to India, South Africa, Brazil), Candle (570 Tbps), and others.

Amazon: Building Fastnet (transatlantic, >320 Tbps, 2028) and partnering on others.

Microsoft: Co-developer of MAREA and investor in multiple transpacific and regional systems.

Owning fiber pairs eliminates leasing costs, enables custom technology (spatial division multiplexing, optical switching), and creates a powerful competitive moat.

3. AI Turns Bandwidth Into Strategic Infrastructure

AI workloads are symmetric, latency-sensitive, and data-intensive. They already represent ~20% of network traffic (projected >30% by 2034) and require roughly 5x the connectivity of legacy topologies. Nokia forecasts ~30% annual subsea bandwidth growth for years.

New cables are engineered for this reality. Their massive capacities (hundreds of Tbps) and advanced features support distributed training and inference at global scale. Subsea capacity and route diversity are becoming gating factors for AI deployment.

4. The Geopolitical Risk Map

Five chokepoints concentrate risk: Baltic Sea, Red Sea/Gulf, Taiwan Strait/South China Sea, Strait of Hormuz, and emerging Arctic routes. Recent incidents — including Chinese vessels in the Baltic and Taiwan, and Houthi attacks in the Red Sea: demonstrate how quickly connectivity can be disrupted.

Governments are responding: stricter U.S. licensing, NATO patrols, EU funding, and restrictions on Chinese equipment. This creates tailwinds for defense, surveillance, and repair sectors.

5. Who Benefits / Who Is Exposed

Direct Winners: Alphabet, Meta, Amazon, Microsoft.

Manufacturing Oligopoly: Alcatel Submarine Networks, SubCom, NEC.

Supporting Layers: Ciena, Infinera, Nokia, Corning (optics/fiber); Global Marine, Orange Marine (vessels); Equinix, Digital Realty (REITs); insurers, defense contractors (Lockheed, Raytheon, etc.).

Exposed: Legacy telecom carriers without ownership, route-concentrated sovereigns (especially Africa/Pacific islands), second-tier clouds, and latency-sensitive financial venues.

6. The Moat: A Durable Competitive Advantage

Subsea ownership creates a physical infrastructure moat with five pillars:

- Cost advantage (no leasing volatility)

- Latency & quality control

- Security & route diversity

- Ecosystem leverage (leasing excess capacity)

- High barriers to entry (capital, permitting, expertise, ship scarcity)

Investment Framework

Core: Hyperscalers + manufacturers + optical/marine leaders.

Second-Order: REITs, power, insurance, defense surveillance.

Hedges: Infrastructure ETFs, green bonds.

Vulnerable: Legacy carriers, concentrated sovereigns, second-tier clouds.

Strategic Winners: Integrated AI-cloud-network stacks, SMART cables, redundant domestic capacity.

Open Questions

- Will governments treat cables as strategic utilities?

- How will insurance/financing evolve with rising sabotage risk?

- Satellites as complement or partial substitute?

- Impact of data localization vs. compute concentration?

- Antitrust risks for cable dominance?

Conclusion

The internet does not float in the ether. It rests on the ocean floor. As AI and digital economies scale, control of these cables is becoming a profound strategic and economic advantage.

Big Tech is transitioning from bandwidth renters to owners of the physical internet. Geopolitical tensions are turning the seabed into a defended domain. For forward-looking allocators, the opportunity is clear: position into the owners, builders, protectors, and enablers of this critical infrastructure.

Final word: The AI cycle is narrated as a story of chips and models. The harder, less crowded, and more durable trade is the layer underneath, who owns the roads connecting the compute. Right now, four companies are buying them, three are building them, and a handful of actors are starting to defend them. Capital should follow.