Neurotechnology Is Leaving the Lab

The Investor Deep Dive on Brain-Computer Interfaces, Human Augmentation, and the Next Platform Shift

The Investor Deep Dive on Brain-Computer Interfaces, Human Augmentation and the Next Platform Shift

Brain-computer interfaces (BCIs) have moved far beyond university labs and sci-fi speculation. Today, we see real human implants, early clinical trials, first regulatory approvals, major funding rounds, sovereign investment, and intense competition across technical approaches.

Yet investors must stay grounded. This is not yet the era of mind uploading or consumer telepathy. The immediate, investable opportunity lies in restoring communication, movement, independence, and cognitive function for people with severe neurological conditions — where clinical evidence, regulatory progress, and reimbursement pathways are building fastest.

The core question: Can BCIs become a durable new class of implantable medical platform, akin to pacemakers, cochlear implants, or deep brain stimulators? The evidence increasingly says yes, but only for companies that master safety, scalability, and real-world utility.

The Market Is Splitting Into Three Strategic Camps

The BCI landscape features competing philosophies:

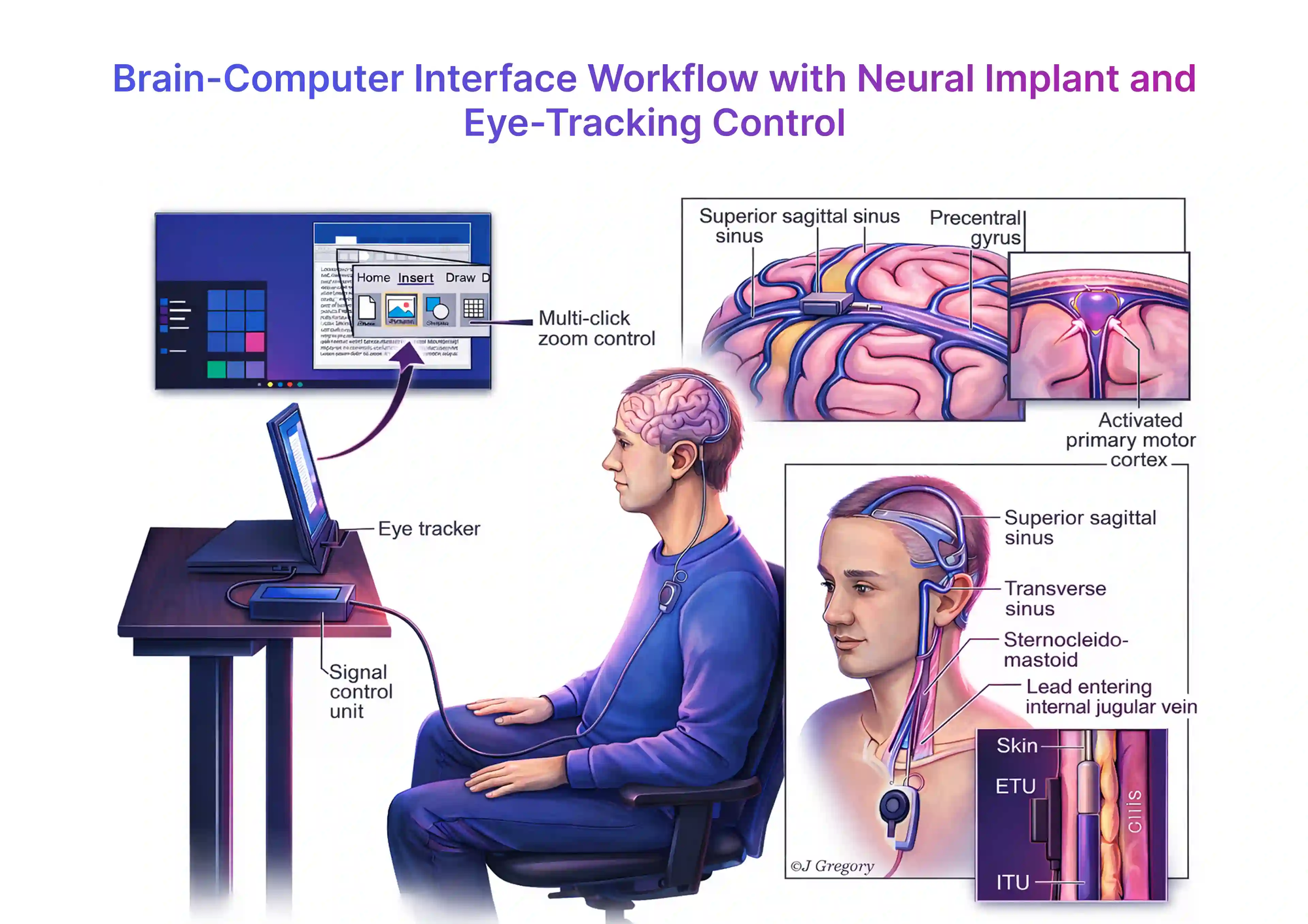

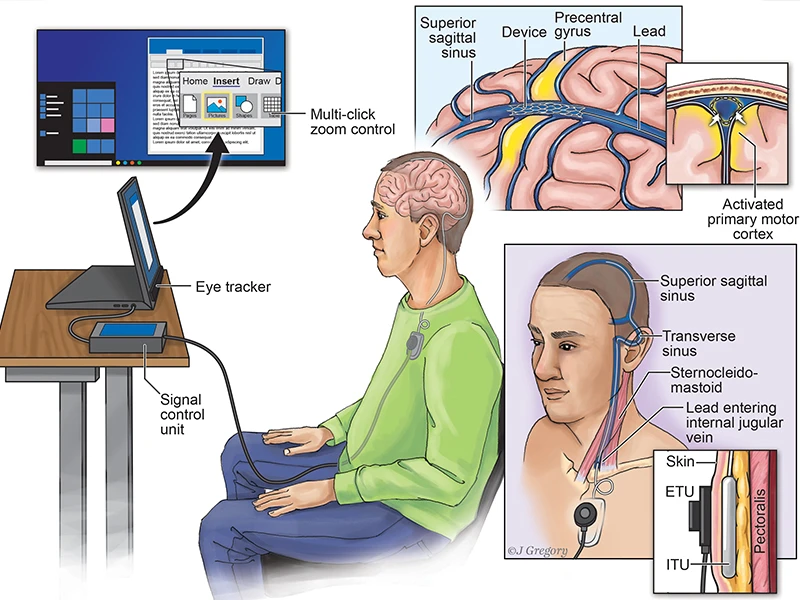

• High-bandwidth camp (Neuralink, Paradromics): Direct cortical implants for the richest neural signals, enabling advanced control and speech restoration.

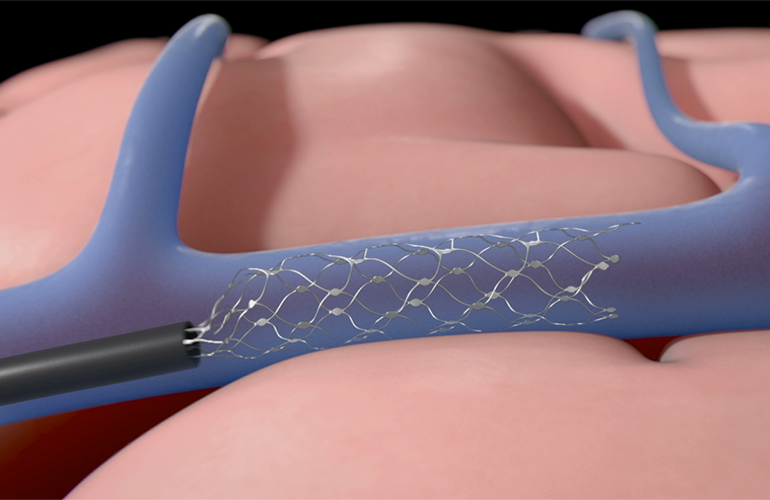

• Procedural scalability camp (Synchron): Endovascular “stentrode” approach via blood vessels, minimizing open-brain surgery and leveraging existing neurointerventional expertise.

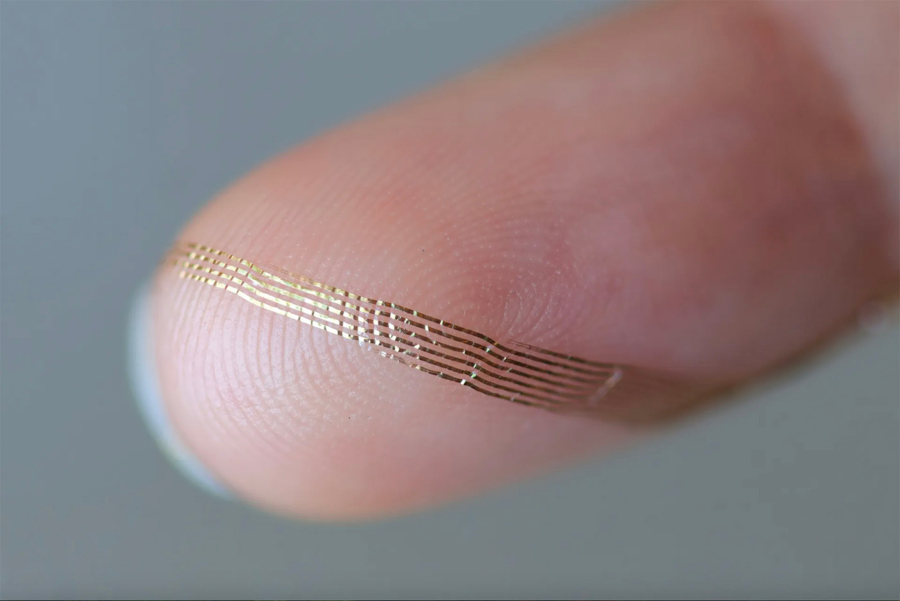

• Tissue-interface camp (Axoft): Ultra-soft, biocompatible materials to solve chronic inflammation and signal degradation caused by mechanical mismatch with brain tissue.

Success won’t go to the company with the most electrodes, but to the one delivering a safe, repeatable, reliable, and economically viable product for years inside real patients.

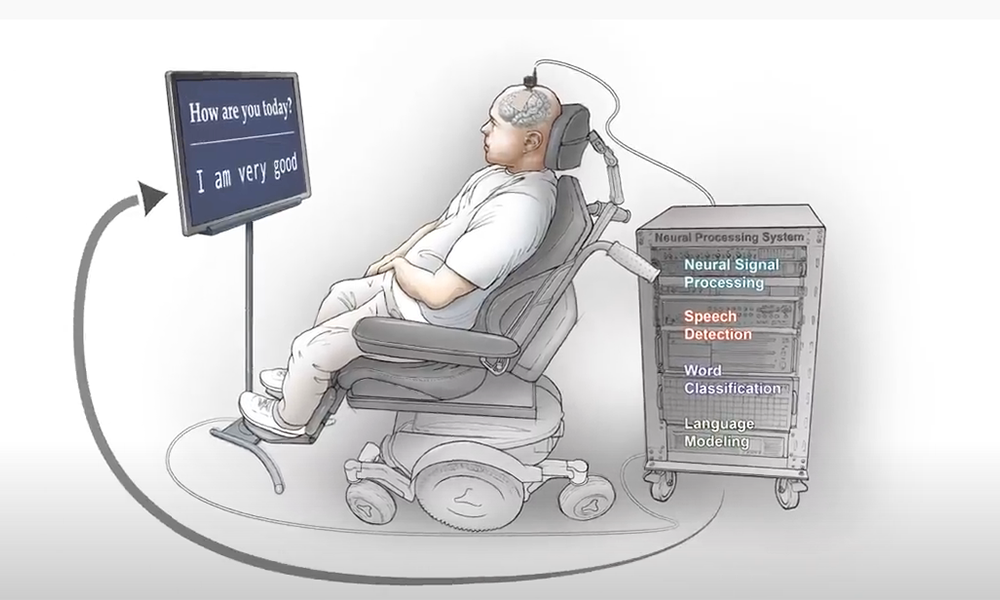

The First Real Market Is Restoration, Not Enhancement

Underwrite restoration first. The strongest early use cases: paralysis, ALS, spinal cord injury, stroke, locked-in syndrome: involve patients who may accept neurosurgical risk for restored independence.

Enhancement (faster typing, thought-controlled apps for healthy users) is the long-term option value, not the near-term business case. The “ChatGPT moment” for BCIs will likely be a paralyzed patient reliably communicating or controlling their environment from home.

Why This Is an Industrial Stack, Not Just a Device

A BCI is a complex system:

1. Neural interface (electrodes/materials)

2. Electronics & amplification

3. Power & wireless telemetry

4. Surgical delivery

5. Adaptive AI decoding

6. Application layer (cursor, speech, robotics, therapy)

Bottlenecks in chronic stability, low-power design, surgical robotics, and decoding algorithms may create the strongest moats: the “ASML of neurotech” could be a hidden layer player rather than a branded implant company.

The Technical Fault Line: Bandwidth vs. Safety vs. Scale

Intracortical approaches (Neuralink, Paradromics) promise highest performance but carry greater surgical and long-term safety complexity.

Endovascular (Synchron) prioritizes easier adoption and workflow fit.

Soft materials (Axoft) aim to improve durability across approaches.

Winners will optimally balance signal quality, procedural risk, clinical outcomes, and economics.

The Near-Term Revenue Model Looks Like Medtech, Not SaaS

Expect upfront procedure + implant revenue, plus recurring services: calibration, updates, monitoring, and eventual replacements. Reimbursement will hinge on proven clinical benefit, reduced caregiver burden, and improved quality of life, classic medtech metrics.

The Three Monetization Phases

1. Restoration (now): Communication, motor control, independence for severe disabilities.

2. Closed-loop therapeutics: Neuropsychiatric applications, cognitive repair, depression, epilepsy monitoring.

3. Augmentation (long-term option): Cognitive enhancement, seamless human-AI symbiosis.

Focus capital on Phase 1 today.

The Timeline: Slower Than Hype, Faster Than Most Realize

2025–2026: Expanded trials and first commercial steps (especially in China).

2027–2030: Narrow approvals in high-need indications in the West.

2030s: Reimbursement, training networks, and real-world durability data will decide scale.

FDA approval is just one milestone — sustained home use is what builds companies.

China Is Moving Faster — and That Changes the Global Race

China is accelerating clinical trials, approvals, and manufacturing. This compresses timelines but introduces geopolitical, data sovereignty, and national-security risks. Western investors will likely apply higher discounts to China-exposed plays.

The National-Security Layer Is Becoming Real

Neural data is uniquely sensitive. Future companies building large decoding datasets must also act as regulated data infrastructure players — with robust cybersecurity, consent, and edge processing.

Competitive Landscape Snapshot

• Neuralink: Highest visibility, vertical integration, robotics, and ambition.

• Synchron: Most pragmatic scaling path via endovascular delivery.

• Paradromics: High-bandwidth focus on speech restoration.

• Axoft: Materials platform with potential category-wide impact.

• China players (Neuracle, NeuCyber, etc.): Speed and state support, with added risks.

Public-Market Exposure: Often Indirect

Pure-play BCIs remain mostly private. Consider established medtech names in neuromodulation (Medtronic, Boston Scientific), surgical robotics (Intuitive), catheter systems, low-power electronics, and AI clinical software for better risk-adjusted access.

The Pick-and-Shovel Opportunity

Highest ROI potential with lower headline risk lies in enabling layers:

• Chronic biocompatible interfaces

• Precision delivery robotics & catheters

• Wireless power & telemetry

• Adaptive decoding algorithms

• Neurosecurity & data infrastructure

These chokepoints are where durable competitive advantages will form.

Bull, Base, and Bear Cases

Bull: BCIs become a major medical platform; rapid AI progress + reimbursement unlock multi-indication growth.

Base (most likely): Important but niche medical category focused on restoration, growing steadily through the 2030s.

Bear: Chronic challenges (signal stability, surgery, regulation) limit adoption to narrow uses.

Investment Conclusion

Neurotechnology has entered its first serious institutional phase. The winners won’t be the loudest storytellers but the companies that solve the hard, “boring” problems: safety, durability, surgery, reimbursement, and long-term patient outcomes.

BCIs are a platform stack and the first great companies in this space will be built by restoring lost abilities to those who need them most. If they succeed, the augmentation future becomes not just possible, but probable. This is one of the most consequential medical and technological frontiers of our time.