The Energy Constraint: Why Electricity, Not Compute, Will Define the AI Decade

Artificial intelligence is no longer constrained by algorithms or chips. It is constrained by electricity.

Compute is scaling exponentially. Model costs are collapsing. Capital is flooding into AI infrastructure at a pace not seen since the early internet. But the physical system underpinning all of it: power generation, transmission, and storage, is scaling linearly at best. This structural mismatch is not a future risk. It is arriving now and it will reshape capital allocation across the global economy for the next decade.

The companies that will define AI's economic trajectory are not the ones building the best models. They are the ones securing the electrons to run them.

The Shift: From Compute Scarcity to Energy Scarcity

For most of AI's modern history, the binding constraint was compute, raw processing power, GPU availability and the cost of training. That constraint is dissolving.

Costs are collapsing across the entire AI stack. Training is cheaper. Inference is cheaper. And as the price of intelligence falls, demand for it expands far faster than efficiency gains can absorb. The system does not shrink, it multiplies. This is the central paradox of exponential technology: lower costs do not reduce consumption. They unlock it.

The consequence is a surge in physical infrastructure demand and the most critical physical input is electricity.

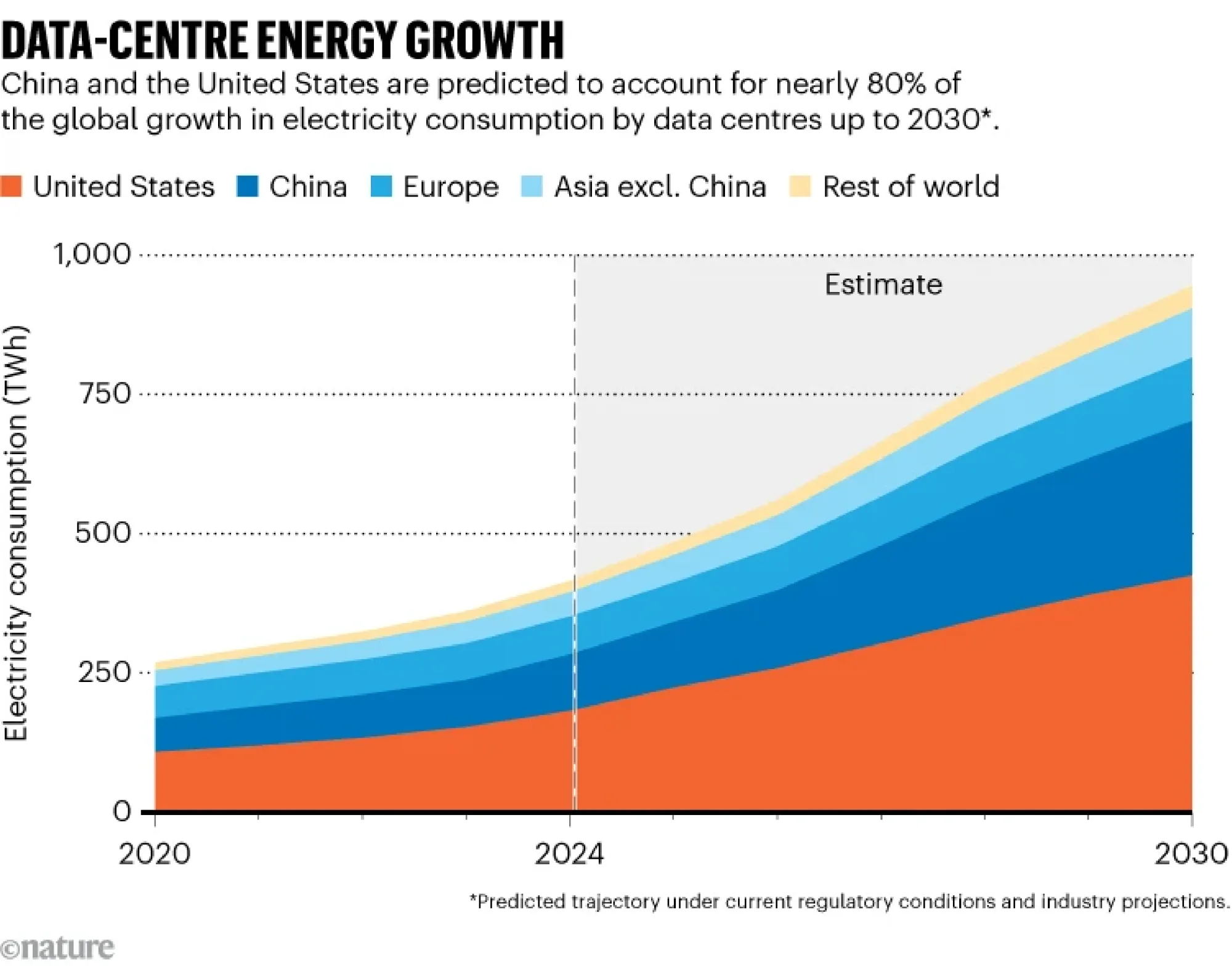

Data centers currently account for roughly 1% of global electricity consumption, a figure that sounds manageable until you understand the trajectory. The IEA projects that number more than doubles by 2030, driven almost entirely by AI workloads. Data center electricity demand is already growing at around 15% annually, five times the rate of the broader grid. At that pace, the energy system is not catching up. It is falling further behind with each passing quarter.

That gap is the investment thesis.

The Grid Is Already Breaking

The bottleneck is not generation. It is transmission.

Power exists. The problem is getting it where it needs to go and that problem is getting worse faster than anyone anticipated. Interconnection queues across the country have gone from long to extraordinary. In Virginia, the epicenter of US data center development, requested grid hookups nearly doubled in the span of six months. Texas regulators have been warned that without major investment, peak demand from AI infrastructure alone could quadruple within a decade. In Singapore, Dublin, and parts of Malaysia, authorities have halted new data center approvals entirely, not for lack of capital or land, but for lack of available power.

The root cause is a timing mismatch that no amount of urgency can easily fix. A hyperscale data center can be designed, permitted, and built in under two years. A major transmission corridor takes a decade. A new substation can take three to five years just to clear permitting. Capital moves at software speed. Infrastructure moves at the speed of concrete and regulatory process.

The result is a widening gap between the AI capacity that exists on paper and the AI capacity that can actually run.

Second-Order Effects: Where the System Breaks

Energy systems do not fail uniformly. They fail at the weakest points. There are five pressure points worth understanding.

Transmission is the immediate bottleneck...

Storage is the second constraint... Short-duration lithium-ion deployments are accelerating, the US installed a record 57.6 GWh of grid-scale batteries in 2025 alone.

Nuclear re-enters the strategic core... Amazon is developing a 960 MW small modular reactor site... Meta has signed agreements for up to 6.8 GW...

Hyperscalers are verticalizing. The most revealing signal... Amazon, Microsoft, Google, and Meta are no longer simply buying electricity. They are building it...

The Economics: Electricity Becomes the Marginal Cost of Intelligence

This has three downstream implications.

First, software margins will increasingly compress toward energy costs.

Second, capital is shifting from software toward infrastructure.

Third, idle grid capacity becomes an asset class.

Investment Framework: Where Capital Will Flow

The energy layer of AI is materially underpriced... The investment opportunity spans three horizons.

Near term (1–3 years): Natural gas infrastructure, flexible generation assets... Grid infrastructure companies... Lithium-ion battery manufacturers...

Mid term (3–7 years): Small modular reactor developers... Long-duration storage...

Long term (10+ years): Nuclear becomes foundational... Fully integrated energy-compute ecosystems...

Structural losers... data center developers who fail to secure power contracts.

The Analogy That Frames the Opportunity

History offers useful precedents. Uranium and nuclear fuel behave today the way early oil did in 1900. Power semiconductors... High-voltage direct current transmission infrastructure is the new cloud backbone.

Closing: The Market Is Looking in the Wrong Place

Investors are focused on models, chips, and applications... But none of that matters if the server cannot turn on.

Every breakthrough in AI increases electricity demand. The companies that secure reliable electricity, will run faster, scale deeper, and compound value longer.

The next trillion-dollar opportunity is not in AI software. It is in building the energy systems that make AI possible.

The market is underpricing that reality. That window will not stay open indefinitely.

The Frontier by Jungle Inc — Research | April 2026