Public Equity Exposure to Artificial Intelligence

An Investor-Grade Framework for Owning the AI Buildout

Executive Summary

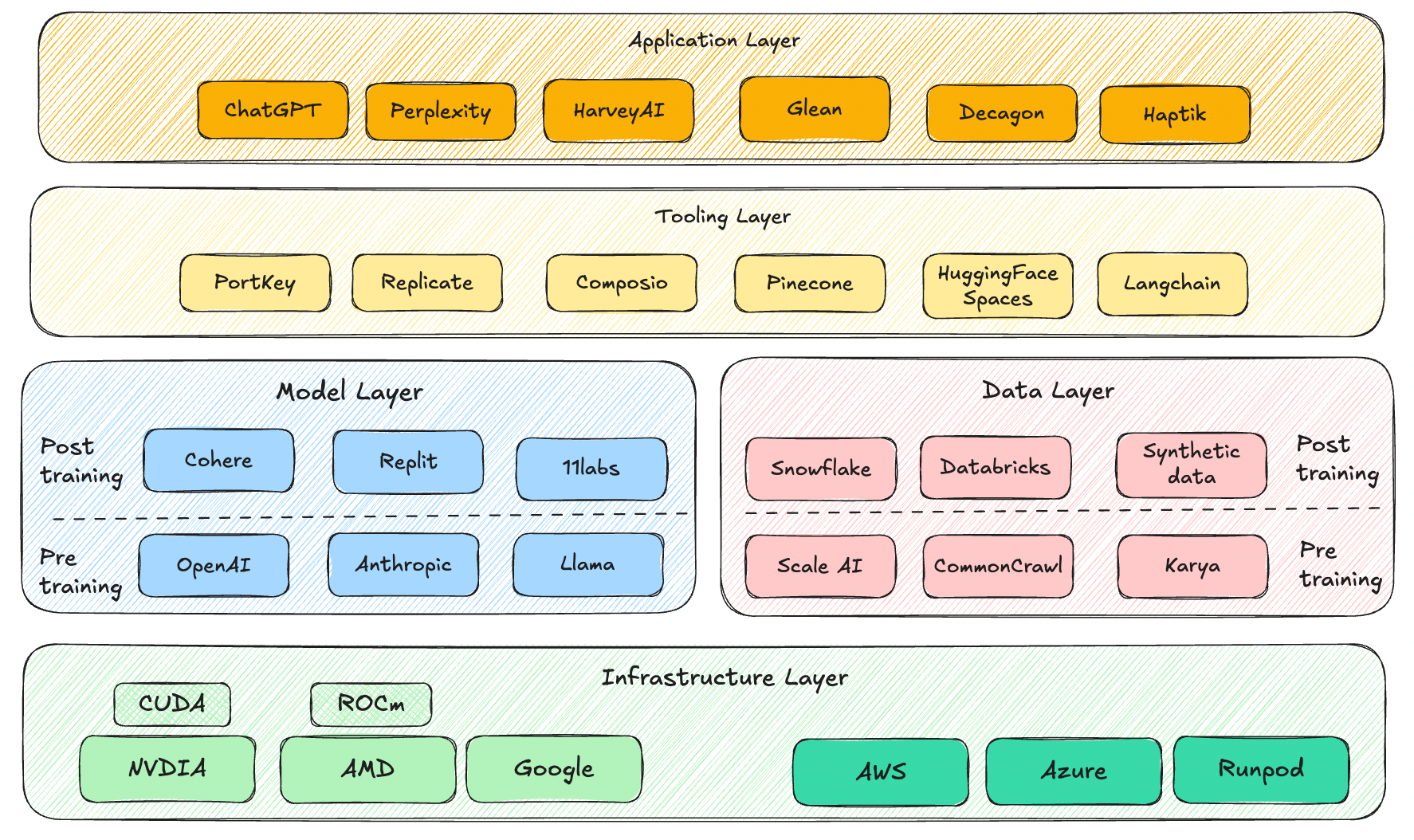

The AI investment opportunity is not a single thematic trade, it is a multi-layer industrial buildout rivaling the scale of past infrastructure revolutions. Value is accruing upstream to those controlling scarce inputs (compute, power, networking), distribution channels, and monetization surfaces. The modern AI stack breaks into four economic layers:

• Compute: Chips, accelerators, advanced packaging

• Infrastructure: Cloud, networking, power, cooling

• Platforms: Models, orchestration, security, data layers

• Applications: Enterprise copilots, automation, consumer AI

Right now, the most reliable, observable profits are concentrated in accelerated compute (GPUs, ASICs), hyperscaler capex, networking, power, and cooling. Application-layer AI remains in price discovery: high engagement, but inconsistent monetization.

Core takeaway: AI is still primarily a capital deployment cycle. Hyperscalers are deploying capital at historic levels: collectively guiding toward $650–700 billion in 2026 capex (up ~60–70% from 2025 levels), with Amazon at ~$200B, Alphabet at $175–185B, Meta at $115–135B, and Microsoft on track for $120B+. This signals the bottleneck remains supply, not demand.

Institutions are quietly owning the infrastructure that powers every AI inference. Retail chases chatbots. The real trade is who collects tolls every time the system turns on.

Market Landscape & Macro Tailwinds

The defining feature of this cycle is capital intensity. Hyperscalers are scaling at unprecedented speed to meet explosive demand for training and inference. Global AI infrastructure markets are projected to grow rapidly (e.g., toward hundreds of billions by 2030), while data center electricity consumption is expected to roughly double by 2030, driven by AI workloads growing ~30% annually.

Key Macro Drivers

As models commoditize, moats shift to data ownership, workflow integration, and distribution control. Infrastructure and platform incumbents retain pricing power.

Large-Cap AI Leaders (Core Holdings)

These companies simultaneously fund and monetize the AI buildout:

• NVIDIA: Compute kingpin—direct monetization of training + inference; FY2026 data center revenue continues explosive growth.

• Broadcom: Custom silicon + networking; AI revenue surging (e.g., Q1 FY2026 up 106% YoY, with strong ASIC and Ethernet exposure).

• Microsoft: Enterprise distribution powerhouse—Copilot, Azure embedded in workflows.

• Amazon: Cloud + custom compute; AWS monetizes AI at massive scale.

• Alphabet: Search + cloud; AI tied to ads and infrastructure.

• Meta Platforms: Consumer distribution; AI boosts engagement and ad efficiency.

• TSMC: Foundry bottleneck for advanced nodes.

Key Insight: These are not interchangeable bets. NVIDIA monetizes scarcity; Broadcom monetizes customization; hyperscalers monetize distribution + recurring spend. The next phase rewards both compute providers and customer gatekeepers.

Mid-Cap AI Enablers (Growth Layer)

Second-derivative plays monetizing every incremental dollar of infrastructure spend:

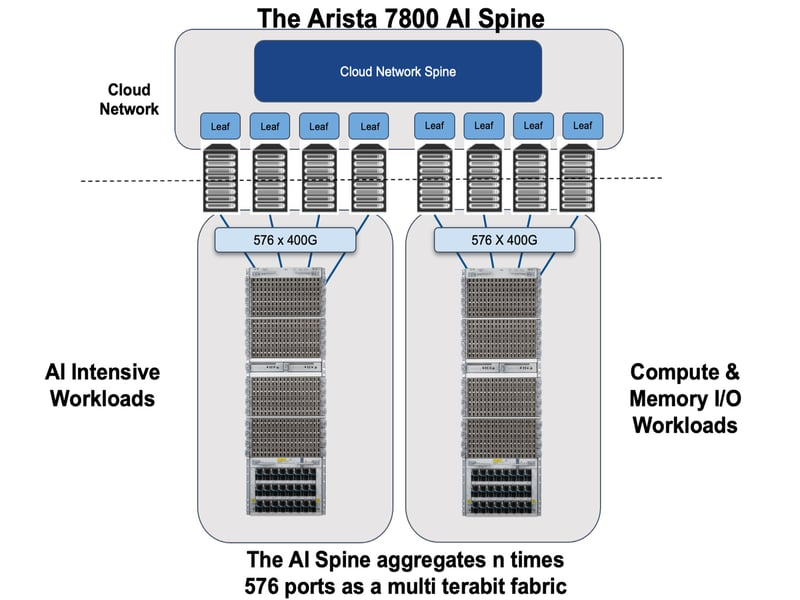

• Arista Networks: AI networking backbone; AI-related revenue doubling in 2026 targets.

• Vertiv: Data center power & cooling; critical for high-density AI racks (liquid cooling surge); strong backlog growth.

Entegris: Chip manufacturing inputs; enables advanced node scaling.

• Symbotic: AI-driven robotics and automation.

These companies sell into AI demand—not “AI products.”

Small-Cap / Emerging AI Plays (Asymmetric Layer)

Disciplined selection is critical. Focus on those with real ARR, embedded workflows, and mission-critical use cases (e.g., UiPath for agentic automation, Five9 for AI-driven CX, Qualys for security, Teradata for data, BlackBerry for edge AI). Avoid narrative-driven exposure without revenue traction.

AI Value Chain Analysis (Where Profits Actually Sit)

AI is a stacked profit system. Every $1 spent on GPUs creates multiple dollars of downstream demand in power, networking, and cooling.

Profit Concentration Map (approximate):

• Compute: NVIDIA, AMD → Highest margins, strongest demand

• Foundry: TSMC → Structural bottleneck

• Cloud: Microsoft, Amazon, Alphabet → Monetization + distribution

• Networking: Arista, Broadcom → Required scaling layer

• Infrastructure: Vertiv, Entegris → Hidden but essential

• Software/Applications: Selective winners only (e.g., Adobe, Palantir)

Ignoring power, networking, and cooling means missing a large part of the margin stack.

Capital Allocation Strategy (3–5 Year Horizon)

Model Portfolio:

• Large Cap: 65% — Stability + direct monetization

• Mid Cap: 25% — Leveraged infrastructure growth

• Small Cap: 10% — Asymmetric upside

Strategic Logic: Large caps fund and monetize AI today. Mid caps capture the multiplier effect. Small caps provide optional convexity. Over 10+ years, power shifts toward distribution owners and workflow controllers.

Risks & Blind Spots

1. Valuation Compression: Strong growth does not guarantee stock performance if expectations are priced to perfection.

2. Hyperscaler Dependence: Many suppliers rely on a concentrated buyer base.

3. Model Commoditization: Shrinking margins at the model layer.

4. Regulatory & Geopolitical Risk: Platform rules, export controls, supply chain concentration (e.g., TSMC).

Top 10 AI Stocks (Long-Term Dominance Framework)

1. NVIDIA

2. Microsoft

3. Amazon

4. Alphabet

5. Broadcom

6. Meta Platforms

7. TSMC

8. Arista Networks

9. AMD

10. Adobe

Hidden Winners (Non-Obvious Plays)

• Entegris → Chip complexity

• Vertiv → Power density

• Qualys → AI in security

• Teradata → Enterprise data

• BlackBerry → Edge AI

Crowded Trades to Approach Carefully

• Pure application-layer AI without distribution moats

• Narrative-driven companies with minimal revenue

• Single-product bets priced for perfection

Final Insight

Retail is chasing AI applications. Institutions are owning the infrastructure.

The real AI trade is not about chatbots. It’s about who gets paid every time AI runs: control of compute, control of distribution, control of capital flows.

The winners aren’t the loudest. They’re the ones quietly collecting tolls every time the system turns on.

This framework positions investors to own the multi-year AI buildout with conviction, discipline, and an edge. The capital cycle is just getting started.