The Musk Empire: A Tesla-SpaceX Merger and the Dawn of Planetary-Scale AI

Elon Musk has never built isolated companies. He constructs interlocking systems aimed at solving humanity’s greatest challenges: sustainable energy and transportation on Earth (Tesla), multi-planetary expansion (SpaceX), and artificial general intelligence in the physical world (xAI, now integrated into SpaceX). With SpaceX’s confidential IPO filing targeting a June 2026 debut at a $1.75–2+ trillion valuation and raising up to $75 billion, the long-speculated full merger of Tesla and SpaceX has moved from rumor to near-inevitability in the eyes of key voices.

Walter Isaacson, Musk’s biographer, stated on CNBC: “I definitely think you’re going to see Tesla and SpaceX end up merging… That’s in his heart. He wants to make this one big company.” Wedbush analyst Dan Ives assigns an 80–90% probability of a merger by early 2027, calling it the “holy grail” for a unified AI-driven ecosystem.

The Current Landscape (Q2 2026)

Tesla remains public with a market capitalization of approximately $1.3–1.4 trillion. Musk’s beneficial ownership sits around 13–20% (including options), a level that has long frustrated his desire for stronger voting control. The company is pivoting aggressively from EVs to AI, robotics (Optimus), autonomy (FSD/robotaxi), energy storage (Megapacks), and Dojo supercomputing.

SpaceX (post-xAI merger) targets a $1.75–2+ trillion IPO valuation after a $1.25 trillion combined post-merger mark. Musk holds ~42–43% equity and ~79% voting power via dual-class shares. Starlink drives recurring revenue (millions of subscribers, defense contracts, direct-to-cell), while Starship advances reusability for Mars ambitions and orbital infrastructure. Tesla already holds indirect exposure via a $2 billion stake conversion from xAI.

Existing synergies demonstrate the convergence:

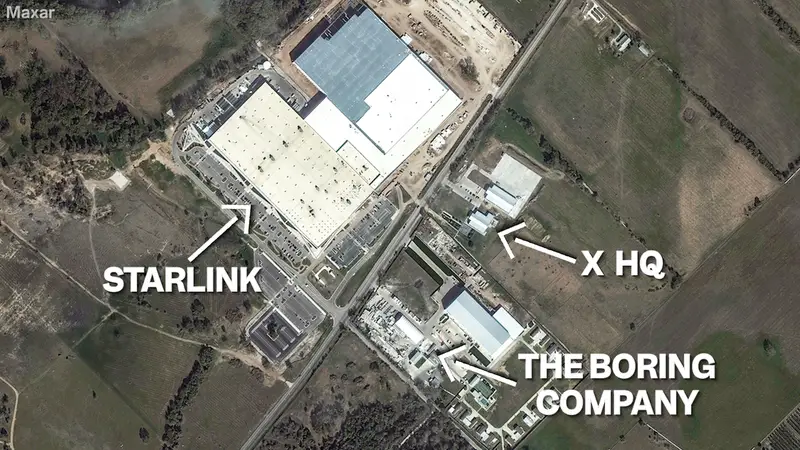

- TERAFAB: Joint AI chip fabrication in Austin, with heavy allocation to SpaceX/space compute.

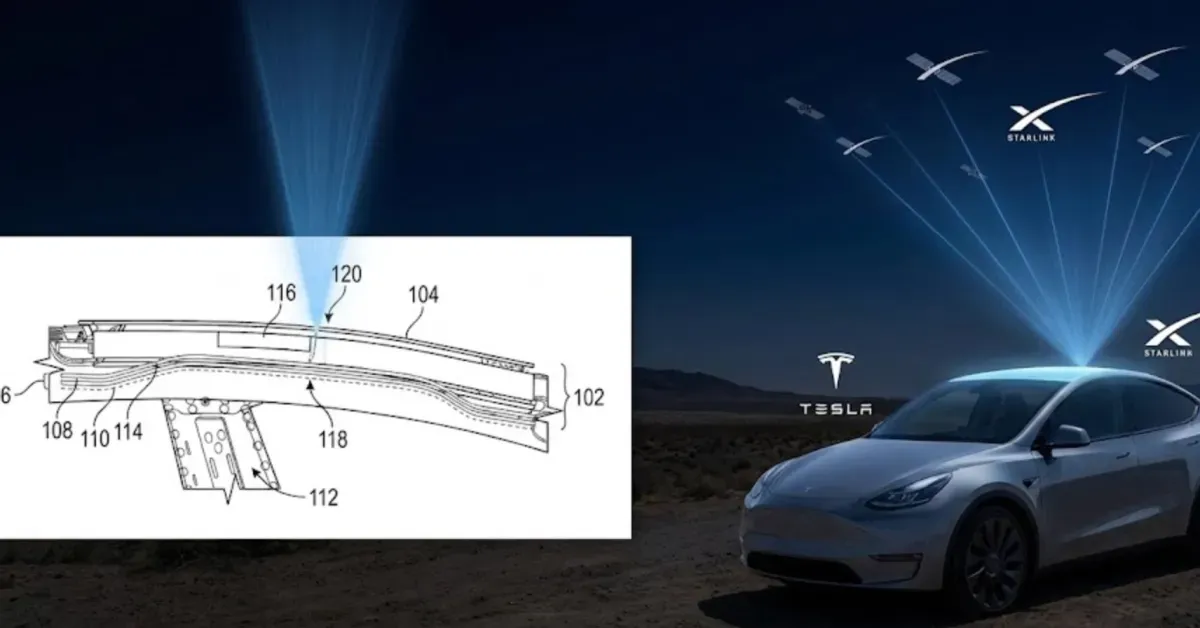

- Starlink integration: Patents and pilots for native connectivity in Tesla vehicles.

- Energy and robotics: Tesla batteries powering SpaceX operations; Optimus robots potentially assembling Starships on Earth and Mars.

The Strategic Case for Merger: Exponential Acceleration

A combined entity could debut at $3–3.5 trillion, creating one of history’s most valuable companies with a singular narrative: “Sustainable Earth-to-Mars Planetary AI.”

Key Benefits:

- Consolidated Control and Capital Allocation — Musk’s effective ownership could rise to ~30%+ with preserved dual-class voting. This resolves Tesla governance friction while directing cash flows (Tesla’s maturing FCF) toward high-upside SpaceX initiatives like orbital data centers and Mars industrialization.

- Vertical Integration at Planetary Scale — Beyond current partnerships:

- Optimus fleets for Starship manufacturing and Martian base-building.

- Unified AI/compute: Dojo + space-based data centers for low-latency orbital training.

- Energy stack: Megapacks powering Starship production, lunar outposts, and AI infrastructure.

- Starlink as the backbone for global Tesla connectivity and future interplanetary comms. ARK-style scenario modeling suggests 20–40% higher compounded growth through eliminated friction and shared R&D.

- Capital Markets and Narrative Dominance — One public behemoth simplifies investor access, attracts sovereign/infrastructure capital, and commands premium multiples. SpaceX’s high-growth multiples (potentially 50–160x on Starlink/AI) could rerate Tesla’s robotics/autonomy story.

- Talent and Operational Efficiency — A single talent pool reduces competition for elite AI, manufacturing, and engineering resources. One governance structure minimizes divided CEO attention.

- Mission Alignment — Isaacson emphasizes this as core to Musk’s psychology. Multi-planetary life demands seamless integration of Earth’s AI/robotics/energy with space infrastructure. Fragmentation risks suboptimal decisions; unification aligns every incentive toward a self-sustaining Mars civilization by mid-century.

Quantified Upside (Hypothetical ARK Framework): Base-case combined revenue CAGR of 35–50%+ through 2030, driven by Starlink monopoly, robotaxi/Optimus scale, and emerging space economy. Bull case: $10T+ market cap by 2035 if a permanent Mars foothold materializes.

The Counter-Case: Significant But Surmountable Obstacles

Musk’s prioritization of undiluted SpaceX control for the existential Mars mission remains a valid concern, as does the ability to extract synergies through partnerships alone.

Major Risks:

- Regulatory and National Security — Highest barrier. SpaceX’s ITAR controls, NASA/DoD sole-source roles, and defense contracts conflict with Tesla’s China manufacturing and global shareholder base. CFIUS review could delay or alter terms significantly.

- Valuation Mismatch and Dilution — SpaceX’s premium (160x EBITDA estimates) risks compression. Tesla shareholders gain upside, but SpaceX holders (including Musk) face dilution. Post-IPO timing is critical.

- Culture and Execution Distraction — SpaceX’s rapid-iteration rocket culture (led by Gwynne Shotwell) versus Tesla’s consumer-facing quarterly pressures. Integration could temporarily slow Starship cadence or Optimus ramp.

- Shareholder and Legal Optics — Potential lawsuits from either side over fairness. Public perception of favoritism.

- No Immediate Necessity — Partnerships (chips, batteries, Starlink, indirect stakes) already deliver substantial value without full consolidation.

Scenarios and Probability Assessment

- Status Quo Partnerships (30–35% probability): Deep collaboration continues without full merger—efficient and low-drama.

- Post-IPO Merger in 2027 (55–60% base case): SpaceX acquires or reverse-merges into Tesla with dual-class protections. High conviction from Isaacson (“definitely”), Ives (80–90%), and precedent (SolarCity, xAI).

- Alternative Structures (5–10%): Enhanced cross-ownership or holding company.

Prediction markets currently price low odds for announcement before end-2026 but rising sharply into 2027.

Investment Implications

For Tesla shareholders: Asymmetric upside from SpaceX exposure at potentially accretive terms, plus validation of Musk’s broader vision. Risks include regulatory delays and short-term dilution optics.

For the broader market: This would represent the ultimate bet on physical AI, space infrastructure, and multi-planetary expansion, far beyond today’s narrow AI narratives.

Final Assessment

The obstacles, particularly regulation and valuation discipline, are real and formidable. Yet Musk’s history of consolidation when it serves the mission, combined with deepening operational ties (TERAFAB as precursor) and explicit commentary from those closest to him, tilts the scales toward execution.

A Tesla-SpaceX merger is not merely corporate engineering. It is the unification of Earth’s sustainable systems with humanity’s insurance policy among the stars. The infrastructure is converging. The vision has always been singular. The stars and the capital markets, appear aligned for one of the most consequential corporate events in history.