The Smartphone Isn't Dying. It's Being Demoted

The Race to Replace It Has Already Started in China.

For the past two years, the AI hardware conversation has swung between two tired extremes: breathless hype that smart glasses and ambient agents will kill the smartphone by 2027, and analyst shrugs that flat shipment numbers prove nothing is changing.

Both takes miss the point.

The smartphone isn’t being replaced. It’s being demoted, quietly, structurally, and in a pattern that echoes exactly how the desktop PC lost its central role after 2010. The PC didn’t vanish. It simply stopped being the sun around which everything orbited. The same fate is now being engineered for the device in your pocket. And the most aggressive moves aren’t coming from Cupertino or Mountain View, they’re already shipping in Shenzhen.

This isn’t a gadget story. It’s an institutional one: about the agent layer, the innovator’s dilemma, and a US-China race that began while Silicon Valley was still arguing over whether the race even existed.

The Graveyard That Keeps the Phone Alive

Start with what failed spectacularly. The clearest proof that the smartphone isn’t going anywhere fast is the pile of “post-phone” devices already buried.

Humane raised $230 million for the AI Pin, a screenless wearable that promised to replace your phone with a cloud AI assistant. It sold roughly 10,000 units before HP bought the assets for $116 million and quietly bricked the devices for existing customers. Rabbit’s R1 orange box, marketed as the “post-app” future, moved 100,000–130,000 units with a reported 95% abandonment rate. Consumers tried them, shrugged and went back to their phones.

These weren’t proofs that the post-phone era is impossible. They were proofs that it won’t happen through abrupt replacement. The winners will be ambient sensors that extend the phone, not standalone gadgets that try to overthrow it.

The Numbers That Explain the Caution

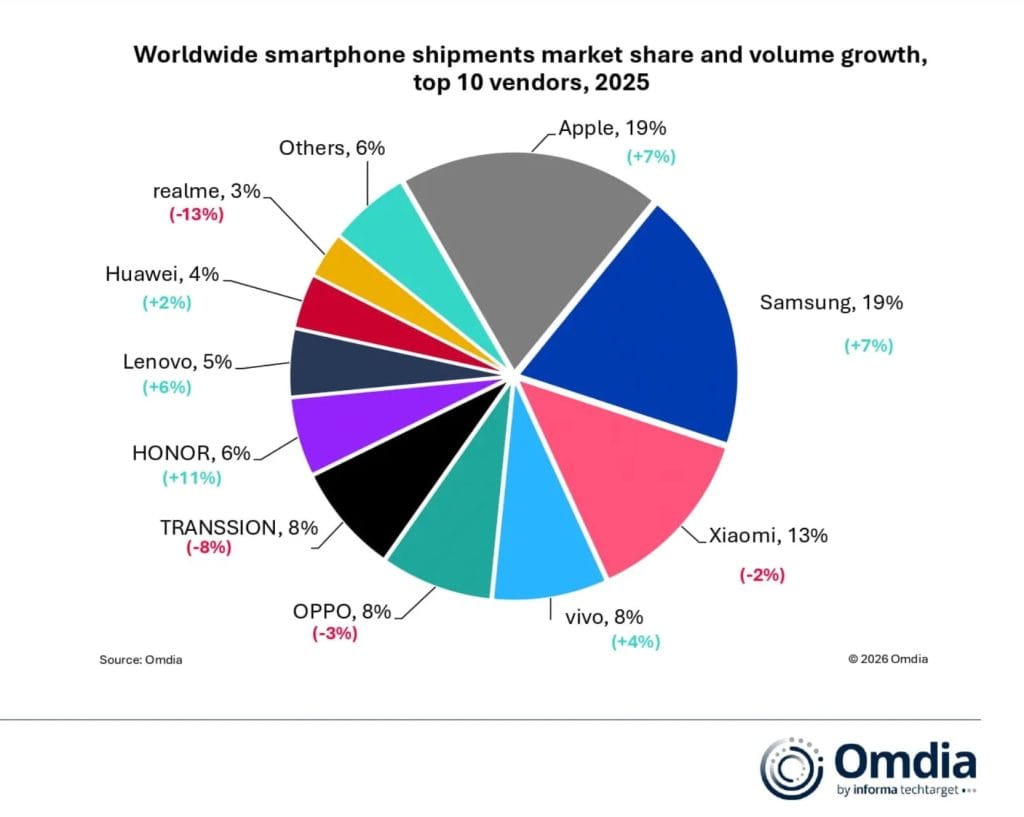

Global smartphone shipments hit approximately 1.26 billion units in 2025, a modest +2% year-over-year. The category isn’t dying; it’s matured into a position of extreme institutional importance.

Apple pulled in $209.6 billion from iPhones in fiscal 2025: 50.4% of its entire $416.2 billion in net sales. Half the revenue of the world’s most valuable consumer tech company still flows through one rectangular slab of glass and metal. That single number is the heaviest constraint in this entire transition. Apple cannot afford to cannibalize its golden goose, so any successor must be architected to protect it, not threaten it.

Meta’s Reality Labs division, the group betting on the next interface, lost roughly $19 billion on $2.2 billion in revenue in 2025. That is the cost of competing for the device that comes after the phone, paid for by the ad dollars the phone still prints.

Replacement cycles have stretched to 3.5 years globally. Battery life, not excitement, drives 75% of upgrades. This is the profile of a saturated, lock-in-heavy market, the exact environment that gets disrupted gradually… until it isn’t.

Apple’s Quiet Hedge: The AirPods Ultra Bridge

While analysts obsess over iPhone refresh cycles, Apple is assembling its most consequential wearable bet in fifteen years and it tells you precisely how the company plans to manage the demotion of its own flagship.

Bloomberg’s Mark Gurman reports Apple is accelerating three new devices: smart glasses (targeted 2027), an AI pendant, and AirPods Ultra launching as soon as September 2026. All three center on Siri. All three use visual context. All three remain tethered to the iPhone.

The AirPods Ultra is the clearest signal yet. Expected to sit above the $249 AirPods Pro 3, it will feature infrared “cameras” (more like Face ID sensors) that scan the wearer’s environment in real time and feed contextual data to Siri without the user having to describe anything.

This is the demotion thesis in hardware form: the earbuds become environmental sensors, Siri becomes the primary interface, and the iPhone quietly shifts into the background compute hub. The screen becomes one surface among many, not the center of gravity.

Apple isn’t building a phone killer. It’s building a constellation of ambient sensors (ears, chest, eyes) that all feed the same assistant while keeping the iPhone as the indispensable anchor. Elegant hedging. But also slow. AirPods Ultra arrives in roughly four months. Glasses are eighteen months out.

This is where China changes the tempo of the entire story.

The Race That’s Already Underway

While Apple spreads cautious bets across three tethered wearables, China is executing a radically different playbook, one born from necessity that has become a structural advantage.

The 2019 U.S. Entity List sanctions cut Huawei off from Google’s Android ecosystem. At the time, it looked like a death blow. In 2026, it looks like the most consequential forced pivot in tech history.

Huawei rebuilt from scratch with HarmonyOS. By the end of 2025, more than 36 million devices ran HarmonyOS 5 and 6, with over 10 million registered developers. In October 2025, HarmonyOS 6.0 shipped with the Harmony Intelligent Agent Framework. Huawei’s central assistant, Celia, now orchestrates tasks across apps and services without the user ever opening them.

The Tiangong Project poured 1 billion yuan ($141 million) into incubating 10,000+ AI-native services, 1,000 intention frameworks, and 5,000 intelligent agents. Early demos show the Xiaoyi Task Space autonomously handling complex workflows, generating a 10,000-word illustrated report in about 20 minutes.

This is agent-native computing at production scale. The phone is no longer the interface, it’s the platform that agents traverse. Intent replaces touch.

Meanwhile, China’s smart glasses market is exploding: shipments projected to top 2.75 million units in 2025 (+107% YoY), on track for 35 million by 2030 at a 47% CAGR. Players include Alibaba, Baidu, Xiaomi, Huawei, RayNeo, Rokid, ByteDance, and even automaker Li Auto. Pricing is aggressive: Alibaba’s Quark S1 at ~$536, G1 at $268, compared to Apple’s $3,500 Vision Pro or Meta’s $799 Ray-Ban glasses. Mass adoption, not premium positioning.

Apple’s first agent-era hardware ships in four months. Huawei’s has been in consumers’ hands for seven.

The Innovator’s Dilemma at Scale

The asymmetry is the analytical key.

Apple and Google are constrained by what they must protect. Apple’s iPhone is half its revenue. Google’s Android powers thousands of OEMs whose businesses depend on the existing app model. They hedge. They augment.

Meta can afford to lose $19 billion a year on Reality Labs precisely because it has no phone or OS rents to defend. Zuckerberg has openly stated AI agents will become the primary way people interact with software, a strategic admission that the agent layer is the next platform war.

Huawei, ironically, has the freest hand. Sanctions stripped away the legacy it would have defended. No Android app store to placate. No installed base to slow it down. The constraint became the catalyst.

The U.S. State Department’s recent $200 million AI Edge Package to fund secure next-gen OSes shows Washington now sees the agentic layer as geopolitical terrain. The public conversation has not caught up.

Six Signals That Actually Matter

The transition is no longer a question of if, only speed, geography, and who owns the agent layer. Watch these six:

- AirPods Ultra traction in its first 18 months. Tens of millions sold = screen demotion accelerates.

- HarmonyOS expansion beyond China — especially into Southeast Asia, Africa, and Latin America.

- Developer behavior shift — agent-first vs. app-first architecture. App Store revenue is the canary.

- Global smart glasses volume crossing 50 million annual units.

- Chinese AI hardware pricing when it hits emerging markets at scale.

- Regulatory frameworks — the EU AI Act, U.S. privacy laws, and Chinese data rules may shape ambient devices more than the silicon does.

The Frame That Reorders the Investment Thesis

Markets are still pricing this as “smartphones with AI features.” The real story is a platform shift in which the smartphone becomes the legacy compute hub feeding ambient surfaces.

The companies best positioned to own the agent economy may not be the ones that dominated the smartphone era. Incumbents are slowed by the very moats they must defend. Challengers unbound by legacy rents can move faster.

The smartphone era was won by the company willing to cannibalize its own products (Apple killing the iPod with the iPhone). The agent era will likely be won by whoever is most willing to make the smartphone secondary and that player may not be headquartered in California.

The phone isn’t dying.

It’s being demoted to the pocket supercomputer that powers the surfaces around us.

Watch the AirPods Ultra launch this September.

Watch HarmonyOS adoption outside China.

Watch where developers start building first.

The next platform war isn’t being decided in keynote slides.

It’s being written in operating system release notes, supply-chain commitments, and the quiet architecture of intent.

The market hasn’t adjusted yet.

It will.