THE TRILLION-DOLLAR PHYSICS FRONTIER

Why the next great infrastructure trade is hiding inside the most expensive science experiment ever proposed

The Frontier by Jungle Inc

There's a phrase that should make every investor sit up straight: "For the first time in history."

CERN, the European physics organization that gave the world the internet, just took a billion dollars of private money. That has never happened. For seventy years, the deepest questions about reality were funded entirely by governments. Then, quietly, in the last eighteen months, the door opened.

The people who walked through that door are not who you would expect, and that is the whole story. Yuri Milner. Eric Schmidt. John Elkann, the man who runs Ferrari. Xavier Niel, the French telecom billionaire. These are not curious philanthropists writing checks to feel important. These are operators who built fortunes on the last three infrastructure waves: internet, mobile, AI compute. They have a track record of recognizing the moment when a piece of public infrastructure is about to become the foundation of a private trillion-dollar industry.

And right now, they are pointing at fundamental physics.

They are not buying physics. They are buying the next generation of accidents.

The Accidents Are the Asset

Here is the only piece of history you need to remember when you read this letter.

In 1989, a software guy at CERN got annoyed that he could not easily share documents with colleagues in other buildings. He wrote a small program to fix his own problem. He called it the World Wide Web. CERN did not patent it. They gave it away. Three decades later, it underpins roughly a third of global GDP.

Nobody saw that coming. Not the physicists, not the funders, not the governments writing the checks. The web was an accident that fell out of a particle physics lab. And it was not the only one.

MRI machines came out of equipment built to study atomic nuclei. Cancer proton therapy came out of accelerator physics. Touchscreens came out of CERN control rooms in the 1970s. The high-field magnets that make today's fusion startups possible were perfected for colliders. Every one of these was unintended. Every one of them now sits at the heart of a multi-billion dollar industry.

This is the pattern. Push instruments hard enough to ask nature its hardest questions, and you build capabilities that the rest of the economy eventually figures out how to monetize. The science is the question. The supply chain is the asset.

Big physics is the only line item in the global economy that has produced a trillion-dollar accident every generation for a hundred years.

The Setup

Three things are happening at the same time, and the timing is what makes this a trade rather than a curiosity.

One. Physics has hit a wall.

The Standard Model, the equation set that describes how matter and forces work, is the most successful theory humans have ever written. It is also incomplete. It cannot explain ninety-five percent of the universe. The stuff we are made of, atoms and stars and planets, is the small visible fraction. The rest is dark matter and dark energy, and we have almost no idea what either is.

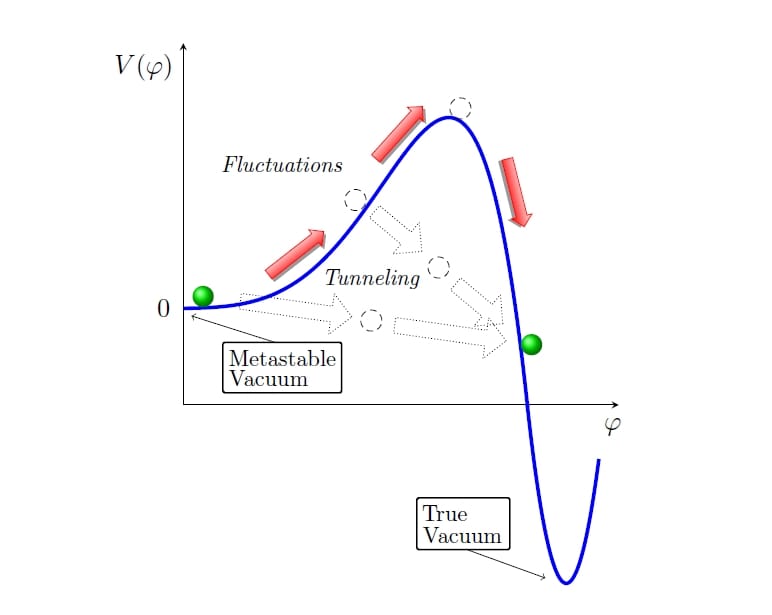

On top of that, the equations themselves carry a strange warning. When you plug in the numbers we have measured, the math suggests that the universe we live in is not sitting in its most stable state. Think of a marble resting in a shallow dip on a hillside. There is a deeper valley further down, and in principle the marble could roll. The expected timescale for that roll is so long it is not a worry, but the fact that the equations are telling us this at all is the point. Our best theory of nature has an asterisk at the bottom of the page, and we cannot read it without a bigger instrument.

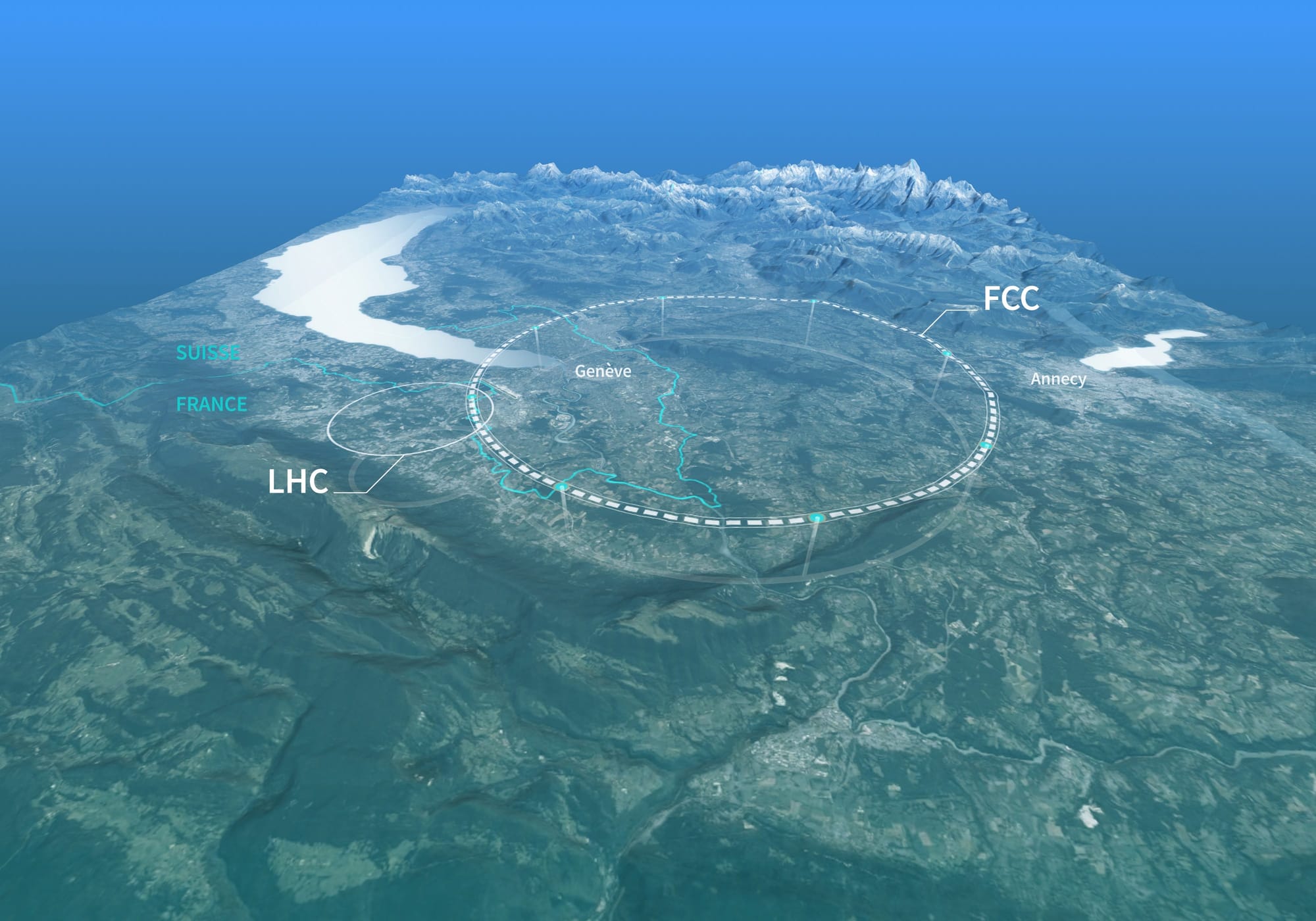

The Large Hadron Collider in Geneva, the most expensive science experiment ever built, has reached the end of what it can do. It found what it was built to find, the Higgs boson, in 2012. After that the discoveries thinned out. Not because the machine failed but because the next questions live at energies and precisions the LHC cannot reach. To go further, you need a bigger ring. A much bigger ring.

Two. Governments cannot pay for the bigger ring.

The next collider, called the Future Circular Collider, will cost roughly seventeen to eighteen billion dollars and take twelve years to build. CERN's entire annual budget is about a billion and a half. The math does not work on the old funding model.

Meanwhile every developed country has the same problem. Aging populations. Defense pressure from a rougher geopolitical environment. Healthcare and pension obligations climbing every year. Discretionary science budgets are the easy thing to trim, and they are getting trimmed. There is no version of the future where Brussels and Washington and Tokyo simply triple their physics outlays.

So CERN did something it had never done. It went looking for private capital.

Three. The right people answered the phone.

This is the part that should make you pay attention. The first billion in private commitments did not come from foundations interested in pure science. It came from people who personally captured the value created by the last two infrastructure waves.

Eric Schmidt ran Google during the period when search and cloud rewrote the global economy. Yuri Milner made his fortune on the early bets in Facebook, Twitter, and Spotify. John Elkann sits on top of the Agnelli fortune and runs Ferrari and Stellantis, two companies whose entire technology stack depends on advanced materials. Xavier Niel built France's largest telecom and is one of Europe's most active AI investors.

These four men have one thing in common. They have all, personally, been on the right side of an infrastructure transition. They know what it feels like when a piece of public good silently turns into private opportunity. The fact that they are now writing checks to a particle physics lab is not random. It is signal.

This Has Happened Before

Step back and the pattern becomes obvious. Every twenty or thirty years, a layer of infrastructure that used to belong to governments migrates to private capital. The pattern is so consistent it is almost boring.

The internet started as a defense project called ARPANET, run by the Pentagon. By the late 1990s the backbone was in private hands and a generation of public-market winners (Cisco, Intel, eventually the cloud giants) emerged from the migration.

Space launch was a government monopoly until roughly 2010. NASA, ESA, Roscosmos. Then SpaceX rebuilt the economics from the ground up, and a private satellite and launch industry that did not exist fifteen years ago is now worth hundreds of billions.

AI compute followed the same arc compressed into five years. Academic and national-lab supercomputers were the cutting edge through about 2019. Then NVIDIA and the hyperscalers took over, and the largest concentration of computational power in human history is now a private balance sheet item.

Each of these transitions made fortunes for investors who saw the migration early and bought the supply chain rather than trying to own the central facility. You did not invest in ARPANET. You invested in the companies that supplied the routers, the chips, the optics, and the eventual platforms. Same with space. Same with AI.

Frontier physics is now starting the same migration. The first private dollars are in. The supply chain is identifiable. The window is open.

The investable surface is never the central facility. It is the supply chain that the central facility forces into existence.

Where the Money Is

A particle collider is, in plain terms, a giant ring made of magnets that pushes tiny particles to nearly the speed of light and slams them together so scientists can see what falls out. Building one requires five very specific things, and each of those things has an existing public-market footprint that any institutional investor can already access today.

The interesting feature is that none of these supply chains exists only for physics. Each of them already has a thriving commercial business, which means demand from frontier physics shows up as upside on top of an existing customer base. This is the part that makes the trade work even if the collider takes longer than expected.

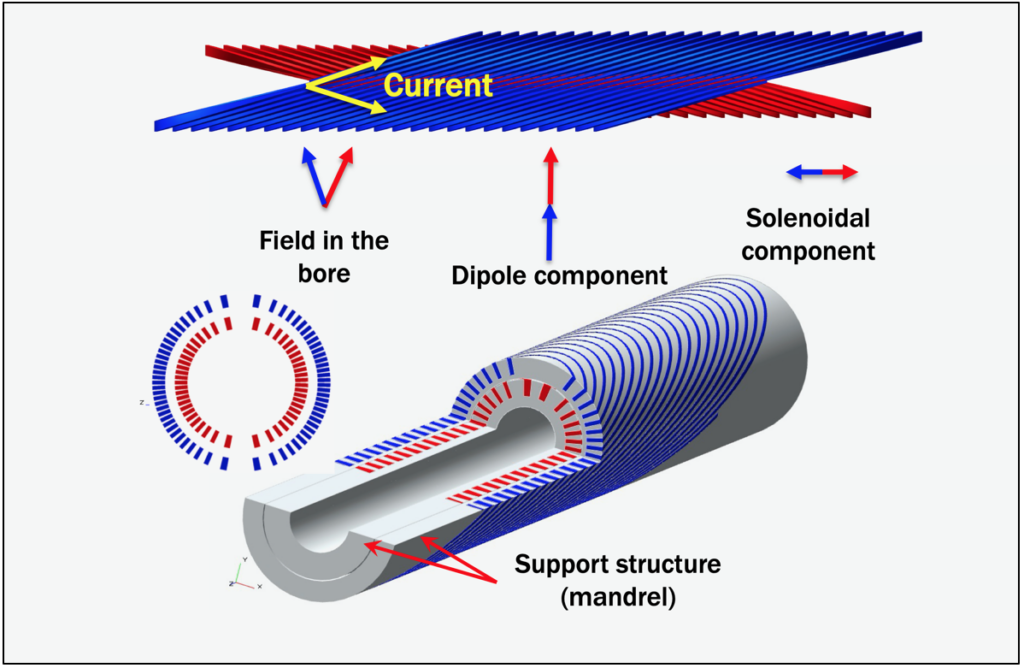

First. The magnets.

The whole machine runs on superconducting magnets. These are also what makes MRI scanners work, what makes the new generation of fusion startups credible, and what is starting to enable a new class of high-density power transmission for cities running out of grid capacity.

There is a quiet revolution underway in this corner. The magnets in the LHC use a material that has to be cooled with liquid helium to nearly absolute zero. A newer class of materials, called high-temperature superconductors, can run hotter, generate stronger fields, and dramatically shrink the size and cost of any system that uses them. The companies racing to scale these materials are positioning themselves to supply colliders, fusion plants, MRI systems, and the next generation of the electrical grid simultaneously.

Public exposures worth tracking include Bruker, Oxford Instruments, Air Liquide, Linde, Furukawa Electric, and Sumitomo Electric. Each of these is already a real business with real cash flow. The collider thesis is the embedded option.

Second. The cameras.

To see what happens when particles collide you need detectors that can register events in trillionths of a second across structures the size of a building. The technology that makes these detectors work has a habit of escaping the lab. The Medipix detector, originally built at CERN, is now inside commercial color X-ray machines that hospitals are starting to deploy. The same fundamental physics, repackaged.

The closely related field of ultra-high vacuum technology — the engineering required to keep a particle beam alive over twenty-seven kilometers without hitting a single stray molecule, turns out to be the same engineering that makes ASML's chip-making machines work. Every advanced semiconductor manufactured today depends on vacuum chambers and precision optics that descend in a straight line from particle physics. ASML is a roughly four hundred billion dollar company. That is not an accident.

Public exposures here include ASML, Hamamatsu Photonics, MKS Instruments, and Atlas Copco's vacuum division (formerly Pfeiffer Vacuum).

Third. The compute.

Modern physics generates absurd amounts of data. The next collider will produce roughly ten times what the current one does and the current one already pumps out tens of millions of gigabytes per year. Sorting through it requires the same infrastructure that powers AI training. Increasingly the same hardware, the same software stack, even the same kinds of neural networks.

The implication is that frontier physics is becoming an additional customer for the AI compute build-out, rather than a separate investment category. Every dollar spent on the collider's data pipeline is, effectively, a dollar spent in the same supply chain that NVIDIA and the hyperscalers already dominate.

Public exposures: NVIDIA, Microsoft, Alphabet, Amazon, and the system integrators like HPE.

Fourth. The power.

A modern collider draws about as much electricity as a small city. The next one will draw more. The bottleneck is not generation, it is the equipment that converts and delivers the power efficiently enough to make the project economic. This is the same problem the AI industry has stumbled into. Hyperscaler campuses are now starting to need gigawatt-class power supplies. The companies that solve high-efficiency power conversion, advanced cooling, and superconducting transmission are about to have not one but two enormous customers.

Public exposures include Siemens Energy, Hitachi Energy, Eaton, Schneider Electric, and Thales.

Fifth. The vehicles that do not exist yet.

This is the most interesting pillar because it is also the least developed. The CERN funding structure — sovereign money, foundation money, and structured private capital all combined into a single multi-decade scientific program — is a template that does not currently exist in clean investable form. We expect the first dedicated frontier science infrastructure funds to launch in the next two to three years. The pattern from climate infrastructure suggests the first vintage of such funds tends to outperform.

This is the pillar where private allocators with access to early vehicles can capture more upside than public-market investors can. It is also the pillar most likely to surprise on the timeline.

What Could Go Wrong

Three honest risks, named clearly.

The first is time. This is a twelve-year construction project that follows a four-year approval process. If your fund cannot tolerate a five-year holding period without a clear catalyst, this thesis is not for you. The supply chain pays carry through its existing commercial business, but the collider-driven upside compounds slowly.

The second is politics. The collider sits underneath France and Switzerland, requires the approval of more than twenty member states, and depends on a level of international scientific cooperation that is fraying. The previous attempt at a mega-collider, the American Superconducting Super Collider, was cancelled by Congress in 1993 after two billion dollars had already gone into the ground. The risk that history rhymes is not zero.

The third is technology substitution. There are several rival concepts for the next generation of particle physics, including muon colliders and laser-driven plasma accelerators. A breakthrough in any of them could redirect spending away from the circular collider design. The good news here is that all of these alternatives draw from the same underlying supply chain — magnets, vacuum, detectors, compute, power. The pillars hold even if the central facility changes shape.

Why Now

Three things are converging on the same window between now and 2028, and they are what turn this from a long-dated curiosity into an actionable trade.

The feasibility study for the collider is reporting this year. Member-state approvals will be voted through 2026 and 2028. Suppliers are already being chosen for the long-lead components, which means the companies that win position now are positioned for a thirty-year demand cycle. By the time the project is officially approved, the supply chain will already be locked in.

The fusion industry is, by accident, paying for the collider's supply chain ramp. Every magnet that Commonwealth Fusion or Helion buys today helps scale the same factories that will eventually serve CERN. The physics customer is being subsidized by the energy customer, which is rare and bullish.

And the AI build-out is doing the same thing for the power and compute pillars. Hyperscaler demand is forcing the kind of grid and cooling investments that frontier physics has been waiting on for two decades. The collider, in effect, is no longer paying full freight for its own infrastructure. It is riding on top of two larger industries that are funding the underlying R&D for their own reasons.

This is the rare moment when a long-cycle scientific project has multiple shorter-cycle commercial industries pre-paying its supply chain. That is what makes the timing matter. Not the date the collider opens. The date the supply chain becomes investable, which is now.

The Last Word

Most investors will read this and assume frontier physics belongs in a separate mental bucket from the investable economy. Beautiful, important, but not really our problem.

That is the wrong frame. The internet was not built to make money. It was built to share physics papers, and it became the foundation of a third of global GDP. The pattern has repeated in space, in compute, and in materials, and it is repeating now in fundamental physics. The difference this time is that capital is showing up before the accident, not after.

The first billion is in. The donor list is one of the most successful investor groups of the modern era. The supply chain is identifiable, publicly traded, and already running real commercial businesses. The next twelve to thirty-six months are when positions get taken.

The deepest questions about reality are about to get answered. The interesting investment question is who finances the asking, and who captures the next round of accidents that fall out.

The deepest questions about reality are about to get answered. The interesting question for us is who captures the accidents that fall out.

Both seats at that table are still open.